The QSuper Defined Benefit can be claimed once you reach your preservation age and have met a trigger of release (e.g. retiring permanently from the workforce).

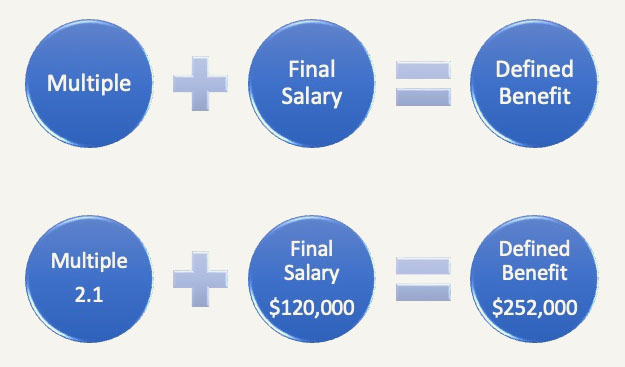

Your defined benefit final balance is calculated at retirement, or when you leave your defined benefit account. Your benefit entitlement is calculated using the following formula that uses your multiple and final salary:

Multiple x Final Salary = QSuper Defined Benefit final balance

Each financial year on the 1st July, your employer will report your salary for superannuation purposes to QSuper. This is what is used to calculate your benefit. Your salary reported is your permanent full-time equivalent salary as at 1st July, including any allowances that have been approved by the Queensland Government. Shift allowances, weekend penalties, and locality allowances are not included.

If your leaving date for your Defined Benefit account occurs on or after turning age 54, your final salary is calculated by averaging your salary for superannuation purposes over the 12-month period before you leave.

The default contribution to your QSuper Defined Benefit is 5% of your salary (for superannuation purposes). You can elect to contribute less, but this means you will have less when you retire.

You can only increase your contributions to your Defined Benefit account above the default 5% via the catch-up provisions. If you are not making catch-up contributions and you wish to contribute more than 5% (5.88% pre-tax contributions), these will need to be paid into an alternative standard super accumulation account either with QSuper or elsewhere.

Yes, your QSuper defined benefit contribution does count towards your annual concessional contribution cap. The amount that needs to be included in your calculation is called your Notional Taxable Contribution (NTC). This is based on a set formula and can also be provided by calling the QSuper Call Centre.

Because your account is part of a Defined Benefit scheme where the QSuper Trustee does not allocate employer contributions to an individual, but instead to a pool, they use a notional taxed contributions (NTC) formula to determine your total concessional contributions (money from your employer standard member contributions that are salary sacrificed money).

This is used to calculate the figure that counts towards your annual concessional contribution cap limit to report to the ATO. It is not as clear as the 5.88% that you make when salary sacrificing. The NTC formula is;

1.2 X [(NECR x 1st July Super Salary) less non concessional standard contributions]

Your employer must contribute the standard 9.5% superannuation guarantee (SG) amount however, if you work for the Queensland Government and make standard member contributions, your employer will contribute up to 12.75% to your super, depending on how much you contribute.

If you work for the Queensland Government, the rate of your standard member contribution sits between 2% and 5%. The rate you contribute will determine the rate your employer contributes. The less you choose to contribute the less your employer will contribute.

Unlike many funds, QSuper’s default investment option is not the same for everyone and instead will depend on your age and investment balance. This is called the Lifetime series of investment options. The option defaulted to, is assessed every six months and adjusted to meet your changing situation when required. There are four options, Outlook, Aspire, Focus and Sustain.

Yes, you can. In addition to the eight Lifetime investment options QSuper has four diversified and four single sector options. There is also a self-invest option for those wanting to invest in shares, term deposits or Exchange Traded Funds (ETFs).

If you would like to arrange a complimentary 15 minute phone discussion to discuss your QSuper advice needs please use the online booking link below.